Earned Value Management

Earned Value Management (EVM) was developed in the late 60s as a Financial Analysis Technique. It became popular in the next four decades as a Project Management Technique. Nevertheless, today it is also known as a Program Management Technique. EVM was adopted by the National Aeronautics and Space Administration of USA (NASA), the United States Department of Energy and the Department of Defense (DoD). In the last three decades has been widely adopted by managers and executives internationally. The ANSI/EIA-748-B-2007 has standardized the use of Earned Value Management Systems (EVMS) that have been adopted in many countries for their procurement programs.

EVM mainly covers the three most important knowledge areas of Project Management: Scope Management, Cost Management and Time Management. EVM unifies those three areas in a common framework that allows mathematically representing the relationship between them. Even though EVM is weak in other areas of Project Management like the Stakeholders Management, it can be used to dramatically improve the success rate in projects when it is complemented with other techniques of Project Management.

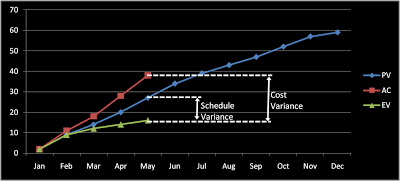

The Actual Cost vs. Planned Cost

If the accumulated actual cost has been greater than the accumulated planned cost, is the project going bad? The common answer is yes, but not necessarily. It depends on the actual progress of the project. The planned cost is related to a measure of progress. If the progress has been very high, an actual cost higher than the planned cost would be clearly justified. A high speed of project execution could have as a consequence a high cost, because the project would ends earlier, with a final cost lower than the planned budget. In ongoing operations, comparisons between actual cost and planned cost are more successful. In schedule based projects, the comparison between actual cost and planned cost would frequently be a mistake, if the progress variable is not included in the analysis.

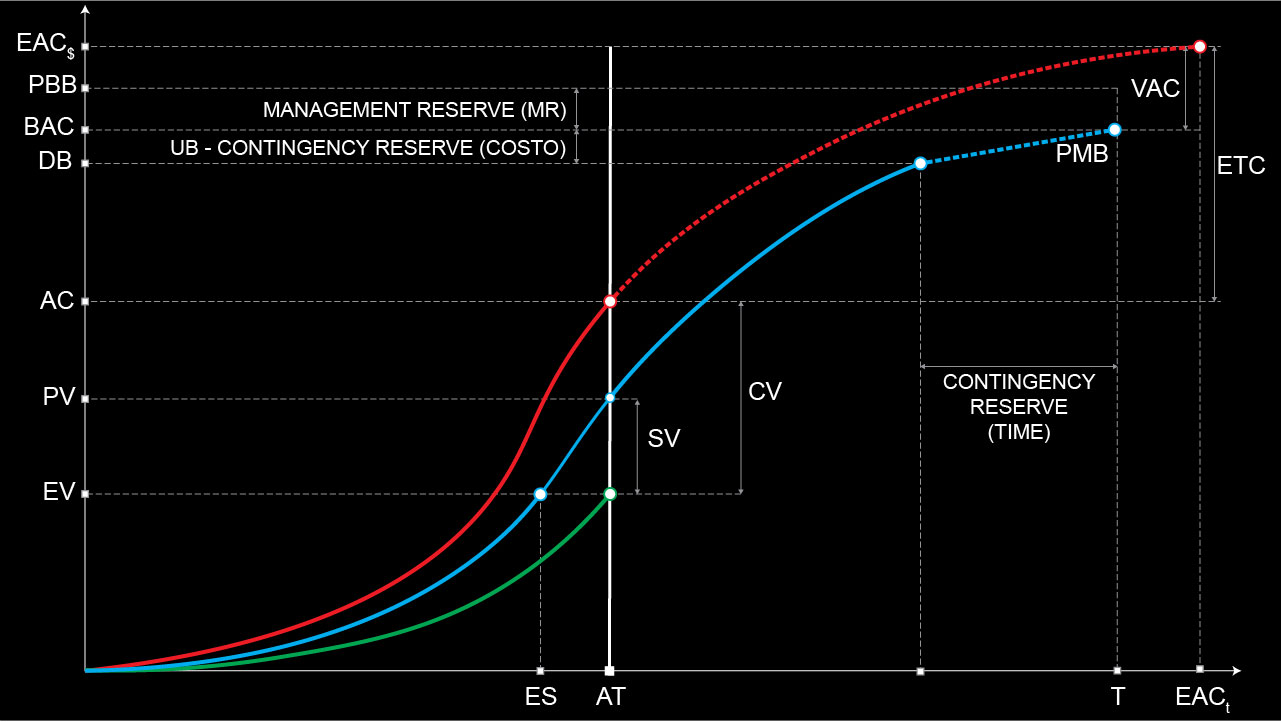

Earned Value Analysis

Earned Value Management is founded in the use of three variables: Planned Value (PV), Actual Cost (AC) and Earned Value (EV). The last variable is a good measure of progress. The Earned Value Analysis mainly compares Planned Value with Earned Value in order to know the speed of the project (SPI y SV). It also compares Actual Cost with Earned Value in order to know if the project is on budget (CPI y CV).